I’ve always wanted an MBA since my days in high school because I thought it distinguished yourself from others but now that an MBA degree is no longer as “sexy” as it was before my reasoning have definitely changed. One of my goals was to get accepted into a top 10 business school, MIT being my focus, but the reasoning behind it was a little naive and selfish. Part of me just wanted to go through because it was MIT!! And also a top 10 which the big Wall Street companies love, apparently. As I’ve gain more knowledge I can see that the opportunity costs are not worth it and now that I have a family, do I want to sacrifice 2 years of watching my daughter grow up to chase a goal that was built on a weak foundation? Also, the end game would most likely result in an increase in my salary but also, most likely, a substantial increase in my hours. With my certain circumstances, I’ve found a perfect solution in pursuing a part-time MBA at Portland State University. This will allow me to stay with my family and also continue working for Turner at the same time, who happens to have a tuition reimbursement program. But the question still remains as to WHY I want to get an MBA and HOW it will benefit my company and my career. It’s also good to write things down so this is my thought process and reasoning behind those prompts.

Knowledge

Here at Turner we don’t sell a product or tangible assets, what we sell is the knowledge, abilities, experiences, and skills of PEOPLE. Therefore if you can improve your staff then you’re only increasing your potential for profitability and ability to sell work. There are a lot of things you can learn on the job and from training but there is also a tremendous amount to learn through course work and interaction with professors and fellow peers in an academic environment. I want to take the holistic approach and add the regiment of academic study to my lessons on business behavior and how a business is ran. By learning about strategies and business theories, I believe I can apply this to my company to find ways we can innovate and improve our processes. The data has shown that construction grows a lot slower than other industries and gaining further knowledge of other sectors and businesses can only help to set my company apart. I believe the knowledge I gain through a graduate business education will give me more perspective and tools to increase the profitability and potential of my company.

Business Relationships

One of the biggest part of business is building relationships and strengthening them because it’s always more fun to do business with someone you know and like and gives you ability to brace and plan if you’re going to do business with someone you might not like so much. From my short time in the construction industry, I quickly found that eventually everybody will know everybody – it’s a small world and there are only a few big players. Being a business class will give me the opportunity to create business relationships with people outside of the construction industry and most likely we’ll be in upper management at our respective companies over the dozen years. Who would you trust building your $40 million office building? Someone who you studied with for countless hours and shared beers with or just some general contractor off the streets? When at business school I’m going to try and create as many relationships as I can because it’ll make the experience more enjoyable and memorable along with providing with a great sound board for the future.

Public Speaking

Without a doubt, if you want to be a big shot at a company then you will need to be a veteran and expert in public speaking. For example, the general manager at my business unit is an amazing public speaker. He never has unnecessary pauses, flows eloquently, uses his hand gestures perfectly with the words, and speaks crisply, cleanly, and very coherently. Every time he speaks I take mental notes to what he does and how he does. I’m sure other people can relate to when you see and hear an excellent speaker talk in front of a large audience – it’s truly a skill that one must master and practice over many hours. Pursuing an MBA will give me many opportunities to practice public speaking whether it’s in large or small groups and will be invaluable experience in my future business career.

Exploring Other Business Industries

My undergraduate degree focused on construction and civil construction and I never really had a chance to learn about other business industries. The MBA’s curriculum will give me a taste into other business industries like finance, private equity, business logistics, global business, product manufacturing, and so many more. I’m very happy being in the construction industry however I would love to delve into finance and private equity a little bit further. I’ve always loved all aspects of business and I think the education will make me more well-rounded by giving me a glimpse of how other industries handle processes/procedures and perhaps I can translate those into the construction industry. I’ve heard many people get an MBA to switch careers but that is not one of the focuses on why I’m getting an MBA – I just want to see what else is out there and if anything else sparks my interest.

These things are what I’m striving for when I go to pursue my MBA – my plan is to apply to PSU before the February deadline and then begin taking my first classes in September 2016. This will also include studying and taking the GMAT which will be difficult with my the current schedule I’m on trying to get debt free but if you want something bad enough, you’ll find a way! I also plan on discussing my goal with my supervisor and upper management this week to get their buy-in for the tuition reimbursement program. The plan actually flows quite smoothly as I’ll just be done with getting debt-free as I enter business school.

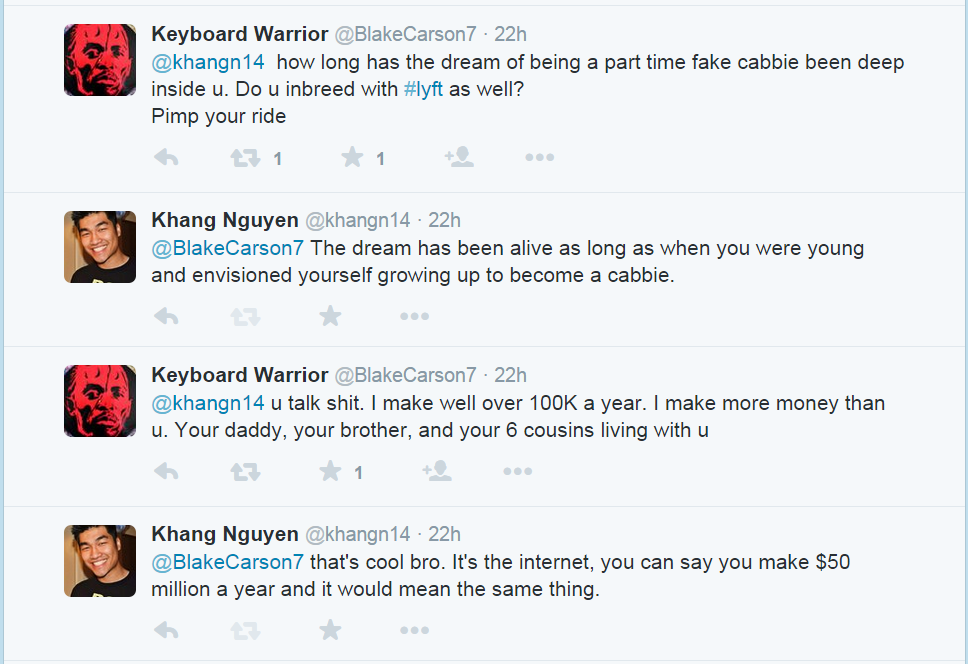

Then the wild troll appeared.

Then the wild troll appeared.

A

A

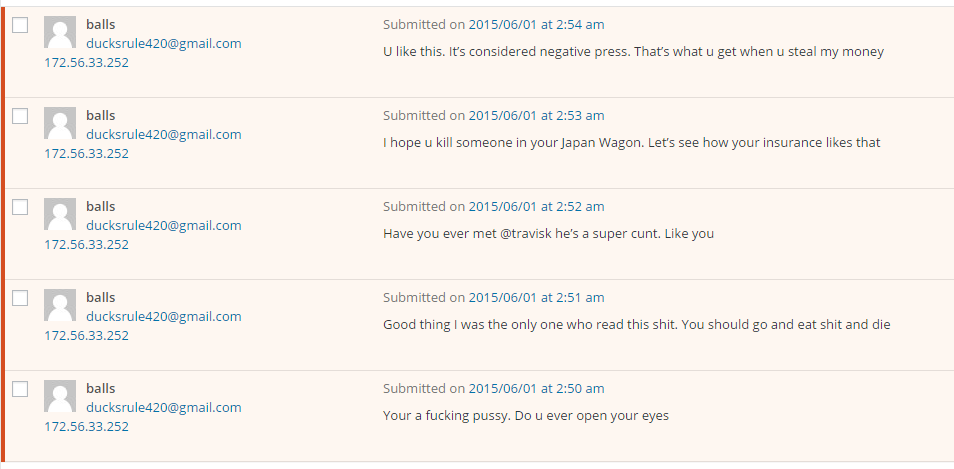

P.S. He then proceeds to post comments on my blog that I chose not to publish. Just goes to show you what people will say when they’re hiding behind their computer screen. FYI, @travisk is the CEO of Uber.

P.S. He then proceeds to post comments on my blog that I chose not to publish. Just goes to show you what people will say when they’re hiding behind their computer screen. FYI, @travisk is the CEO of Uber.

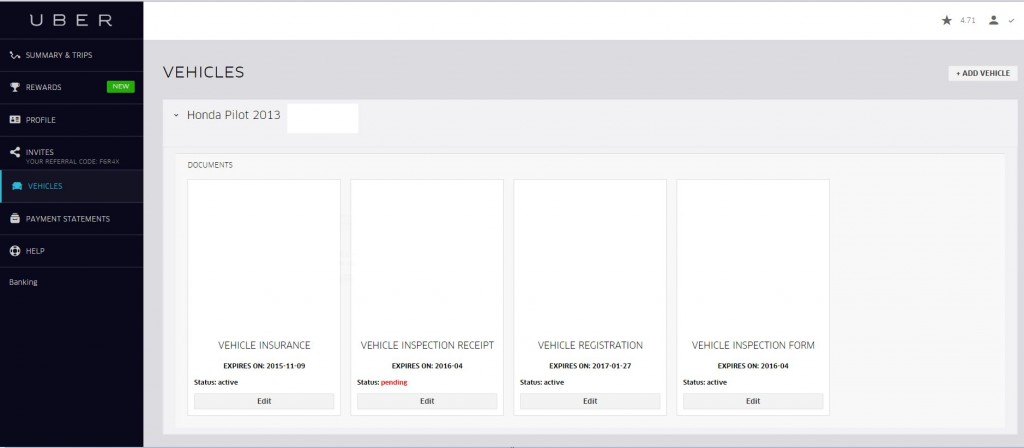

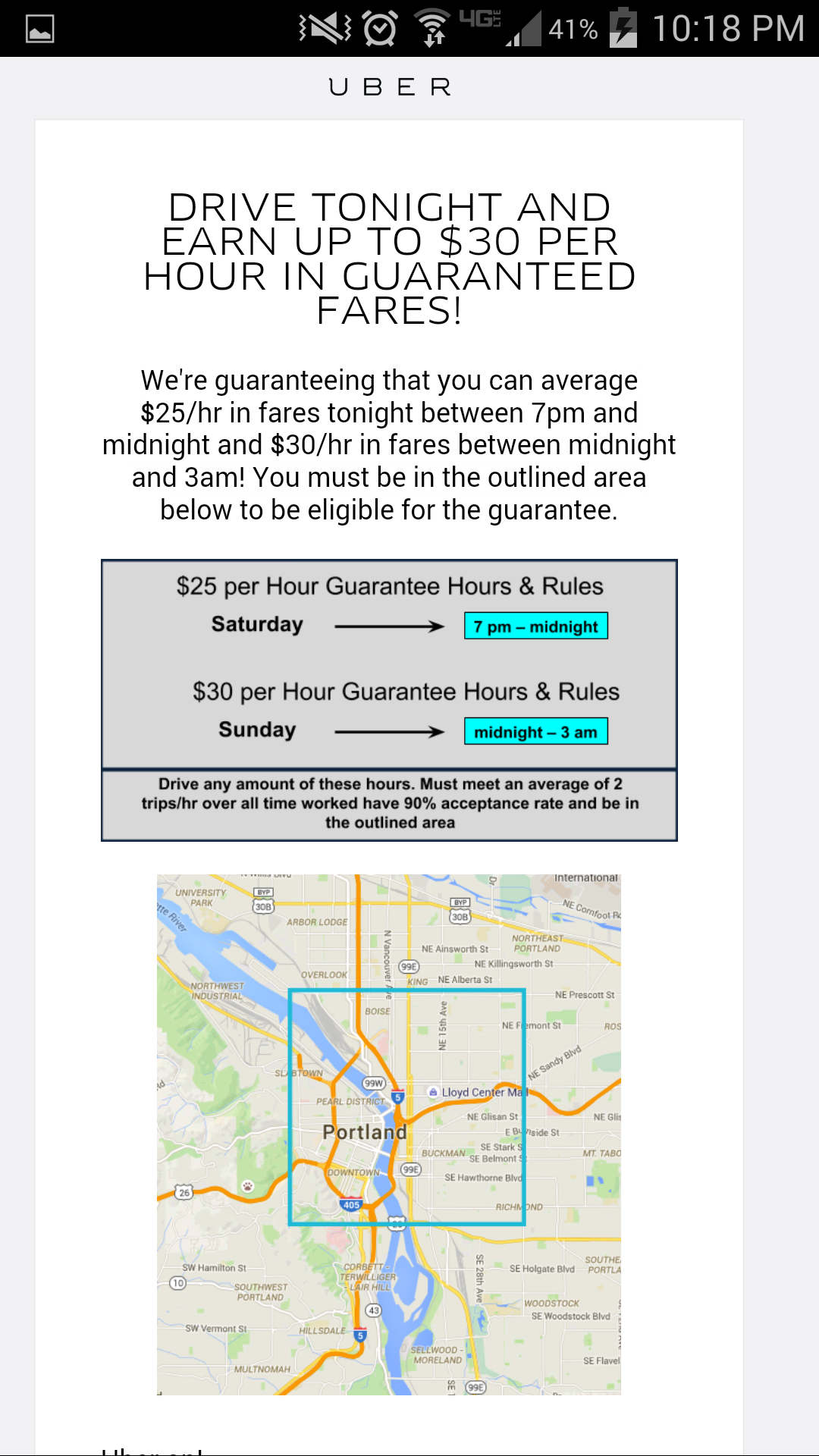

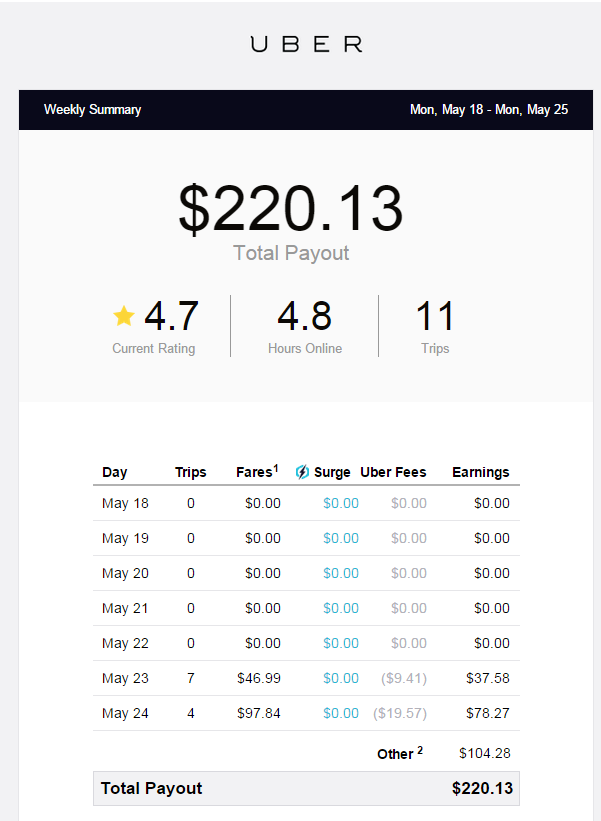

Uber will also run a background check and you can request to be cc’d on the documents (which I did) to see what the cops are saying about you! The check includes driving history along with a criminal scan. They’ll also put a small deposit into your checking account to validate it for direct deposit – mine was a $0.01 deposit. The background check will take 5-7 business days while the document review usually takes 24 hours. The whole process itself took 3 weeks for me with the most difficult part being getting the vehicle inspection completed around my work schedule. Once Uber checks that you’re all good to go they’ll send you a link to download the Uber Partner app and activate your account.

Uber will also run a background check and you can request to be cc’d on the documents (which I did) to see what the cops are saying about you! The check includes driving history along with a criminal scan. They’ll also put a small deposit into your checking account to validate it for direct deposit – mine was a $0.01 deposit. The background check will take 5-7 business days while the document review usually takes 24 hours. The whole process itself took 3 weeks for me with the most difficult part being getting the vehicle inspection completed around my work schedule. Once Uber checks that you’re all good to go they’ll send you a link to download the Uber Partner app and activate your account.

This is a lesson I learned from wanting to play different hero classes and didn’t want to trudge through finding/trading items as I leveled up. I was lucky to be in a position where I could fully furnish any character I wanted with just a few days of trading. For every new character I created, I did extensive research on what the best items, builds, skill sets, and attribute allocations were. I searched forums, talked to players in-game, and ultimately modified the build according to my own knowledge of the game. Therefore, as soon as my character was created and “rushed” I was able to hit the ground running and didn’t waste time learning how the character worked, I already had everything planned and figured out from the start. This lesson has transcended to my everyday life where I do extensive research and calculations before I begin any time consuming task or something that has any risk aspect.

This is a lesson I learned from wanting to play different hero classes and didn’t want to trudge through finding/trading items as I leveled up. I was lucky to be in a position where I could fully furnish any character I wanted with just a few days of trading. For every new character I created, I did extensive research on what the best items, builds, skill sets, and attribute allocations were. I searched forums, talked to players in-game, and ultimately modified the build according to my own knowledge of the game. Therefore, as soon as my character was created and “rushed” I was able to hit the ground running and didn’t waste time learning how the character worked, I already had everything planned and figured out from the start. This lesson has transcended to my everyday life where I do extensive research and calculations before I begin any time consuming task or something that has any risk aspect. Photo sources:

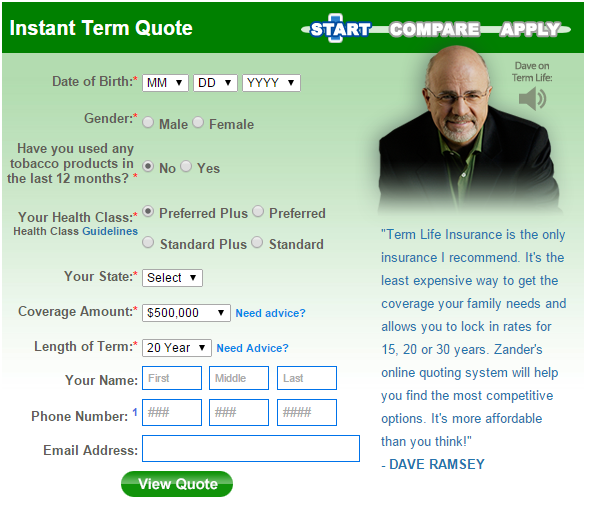

Photo sources: The second question is, “what type of insurance should I get?”. The two most widely used out there is Whole Life and Term Life insurance. Whole Life provides you with a coverage amount you set and a higher premium where the additional dollars above your premium goes into an account that builds your “equity”. Dave Ramsey does not approve this method as you can make more money by taking those additional dollars and invest it yourself. Also, life insurance is not needed for your “Whole” life because as soon as you become fairly wealthy then your family should be financially stable enough to handle any money issues. Term life insurance is similar to car insurance where you pick an amount of coverage and a “term” of how long you want the insurance for. This is the one that I went with because, as I mentioned before, you shouldn’t need life insurance for the rest of your life and it provides the best option with the lowest premium.

The second question is, “what type of insurance should I get?”. The two most widely used out there is Whole Life and Term Life insurance. Whole Life provides you with a coverage amount you set and a higher premium where the additional dollars above your premium goes into an account that builds your “equity”. Dave Ramsey does not approve this method as you can make more money by taking those additional dollars and invest it yourself. Also, life insurance is not needed for your “Whole” life because as soon as you become fairly wealthy then your family should be financially stable enough to handle any money issues. Term life insurance is similar to car insurance where you pick an amount of coverage and a “term” of how long you want the insurance for. This is the one that I went with because, as I mentioned before, you shouldn’t need life insurance for the rest of your life and it provides the best option with the lowest premium.

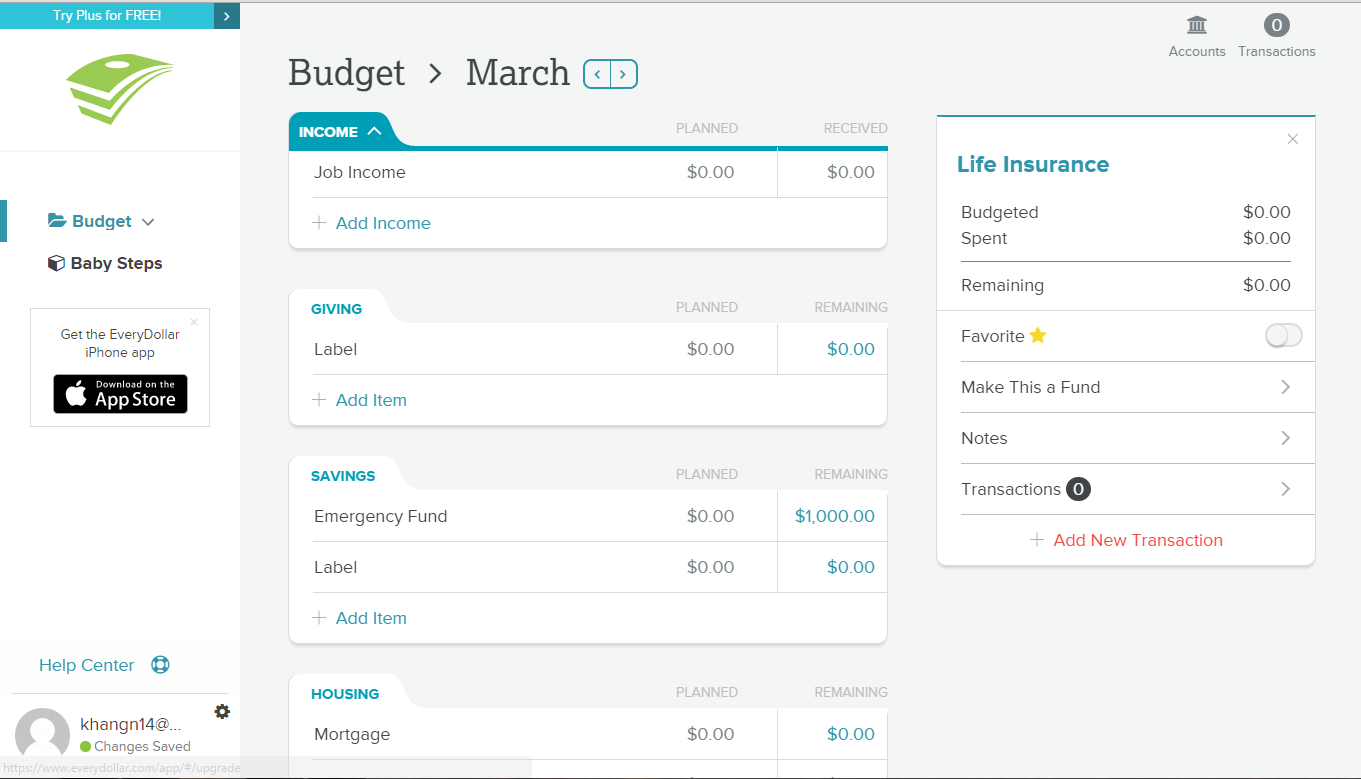

Driver’s License

Driver’s License The website itself is very beautiful and easy to navigate as you can see below. Categories are very cleanly separated with a distinguished tab to help you differentiate between your budget items; the initial category is your income where your budget should start and the default categories are giving, savings, housing, transportation, food, lifestyle, insurance & tax, and lastly your debt. These categories then have smaller sub-categories where you can add your own custom budget line item. An extra item they have on the side is the “Baby Steps” which is Dave Ramsey’s steps to becoming financially wealthy and I think it’s a nice touch but seems a little weird to me that it’s included in the tool – but it’s his budgeting tool so how could he not sneak it in there??

The website itself is very beautiful and easy to navigate as you can see below. Categories are very cleanly separated with a distinguished tab to help you differentiate between your budget items; the initial category is your income where your budget should start and the default categories are giving, savings, housing, transportation, food, lifestyle, insurance & tax, and lastly your debt. These categories then have smaller sub-categories where you can add your own custom budget line item. An extra item they have on the side is the “Baby Steps” which is Dave Ramsey’s steps to becoming financially wealthy and I think it’s a nice touch but seems a little weird to me that it’s included in the tool – but it’s his budgeting tool so how could he not sneak it in there?? The initial step is to put in your monthly income and then move down the line to fill out all you budget items. A nice feature is that as you scroll down the screen, the amount that you have left to budget is locked at the top for you to see. You can also click on the remaining amount and that will toggle the website to switch to how much you’ve spent in your budget. This gets a little annoying because I thought I could change the spent amount by clicking it but I can only do that through the added transactions. Speaking of the transactions, this is where the budget tool fails miserably and makes it no better than a mediocre tool.

The initial step is to put in your monthly income and then move down the line to fill out all you budget items. A nice feature is that as you scroll down the screen, the amount that you have left to budget is locked at the top for you to see. You can also click on the remaining amount and that will toggle the website to switch to how much you’ve spent in your budget. This gets a little annoying because I thought I could change the spent amount by clicking it but I can only do that through the added transactions. Speaking of the transactions, this is where the budget tool fails miserably and makes it no better than a mediocre tool.

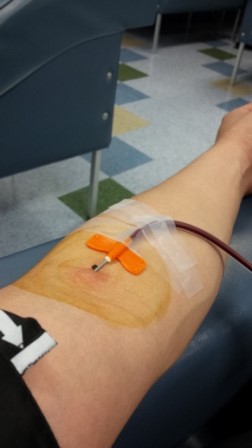

After you complete your questionnaire at the kiosk you will sit down in a lobby or wait in line until you’re called by a technician to complete your shortened health screening. Below is a picture of the lobby of the place I used to donate at in Portland. I’ve covered the face of the individuals to protect their privacy.

After you complete your questionnaire at the kiosk you will sit down in a lobby or wait in line until you’re called by a technician to complete your shortened health screening. Below is a picture of the lobby of the place I used to donate at in Portland. I’ve covered the face of the individuals to protect their privacy.

You’ll quickly find out that they ask for your full name and last 4 digits of your social security very often. Not sure if this is to verify if you’re the same person (I know, I know…) or to make sure you’re still thinking properly and not high off your ass. You can’t see in the photo above but there is a scale just behind the chair and that is what they’ll have you do first. This is important because there are 3 ranges for the amount of plasma you have to donate correlating to your weight – I weighed around 160 and was in the middle band which required me to donate 880 ML. At some centers you get more/less money (+/-

You’ll quickly find out that they ask for your full name and last 4 digits of your social security very often. Not sure if this is to verify if you’re the same person (I know, I know…) or to make sure you’re still thinking properly and not high off your ass. You can’t see in the photo above but there is a scale just behind the chair and that is what they’ll have you do first. This is important because there are 3 ranges for the amount of plasma you have to donate correlating to your weight – I weighed around 160 and was in the middle band which required me to donate 880 ML. At some centers you get more/less money (+/-

After you near the end of your donation, they’ll either give you a saline pack through the IV or make you drink a bottle of electrolytes (Powerade or Gatorade) to help you replenish the fluids you’ve just lost. After that you’re all done and you get paid!

After you near the end of your donation, they’ll either give you a saline pack through the IV or make you drink a bottle of electrolytes (Powerade or Gatorade) to help you replenish the fluids you’ve just lost. After that you’re all done and you get paid!

{kind=link}